- Free Consultation: 866-966-5240 Tap Here To Call Us

What Is Uninsured Motorist Coverage? UM/UIM Explained in CA

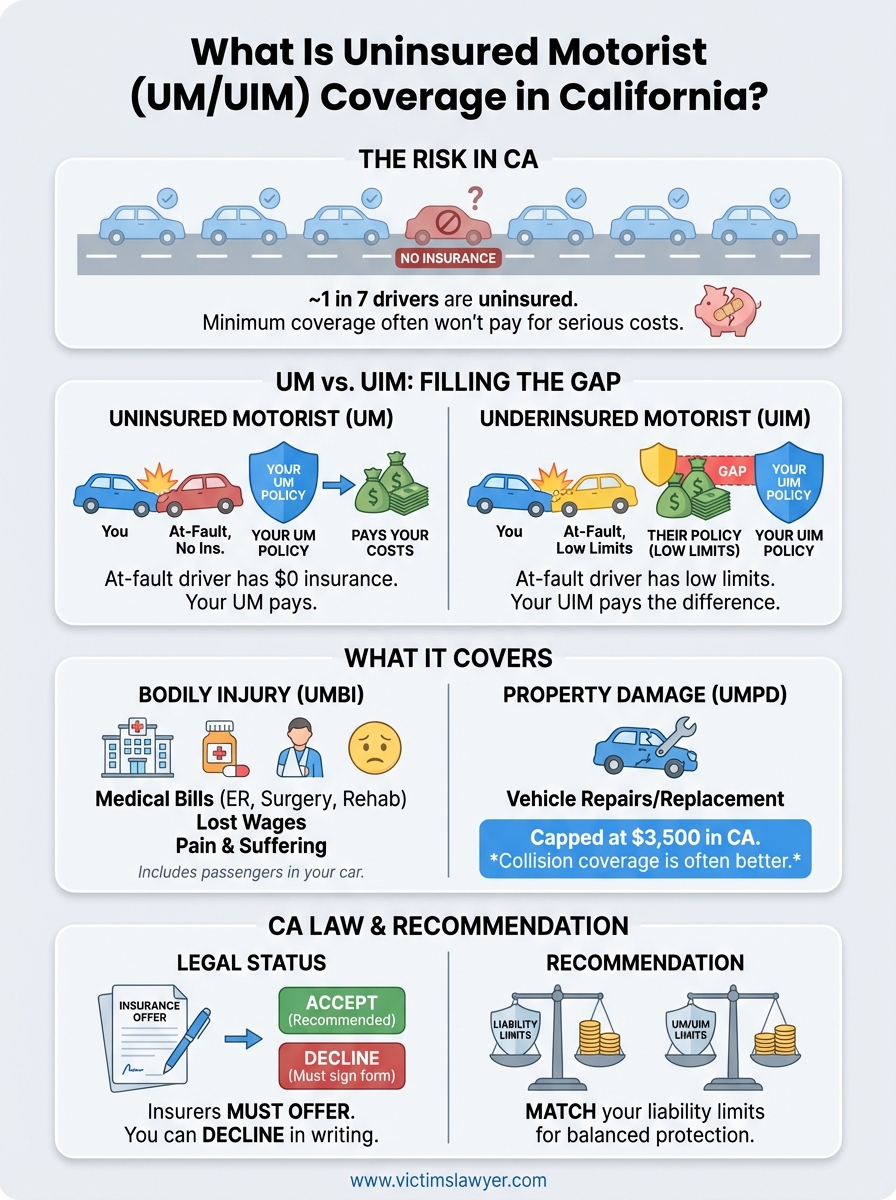

Getting hit by a driver who has no insurance, or not enough of it, can leave you facing thousands of dollars in medical bills with no clear path to recovery. That’s where understanding what is uninsured motorist coverage becomes essential. In California, roughly 1 in 7 drivers operates without proper insurance, meaning your chances of encountering one are higher than you might expect.

This guide breaks down UM/UIM coverage: what it includes, how it works in California, and whether you’re legally required to carry it. At Steven M. Sweat, Personal Injury Lawyers, APC, we’ve spent over 25 years helping accident victims across Los Angeles recover compensation when at-fault drivers can’t pay. Knowing your coverage options before an accident happens can make the difference between financial hardship and a full recovery.

Why UM and UIM matter in California

California’s roads present a specific financial risk that many drivers don’t prepare for. When you’re injured by someone without insurance or with minimum coverage, you face a harsh reality: the at-fault driver can’t pay for your damages, and you’re left covering the gap yourself. Understanding what is uninsured motorist coverage protects you from this exact scenario.

The uninsured driver problem in California

California requires all drivers to carry liability insurance, but enforcement remains imperfect. The state’s uninsured motorist rate hovers around 14 to 17 percent, meaning roughly one in every six drivers on the road breaks this law. You could follow every traffic rule and still get hit by someone who has zero insurance to cover your medical bills, lost wages, or vehicle repairs.

Even when a driver carries insurance, California’s $15,000 minimum bodily injury limit per person rarely covers serious accident costs.

What happens without UM/UIM protection

Medical treatment for accident injuries in California escalates quickly. A single emergency room visit can cost $3,000 to $10,000, and that’s before you factor in surgeries, physical therapy, or ongoing care. Without UM/UIM coverage, you’ll either pay these expenses out of pocket or pursue a civil lawsuit against someone who likely has no assets to claim. Your health insurance may cover some costs, but it won’t replace lost income or compensate you for pain and suffering.

Underinsured motorist coverage fills the gap when the at-fault driver carries insurance but not enough to cover your full damages. A $50,000 medical bill against a driver with $15,000 in coverage leaves you with $35,000 in uncovered expenses unless your own UIM policy steps in.

What uninsured motorist coverage pays for

When you’re asking what is uninsured motorist coverage, you need to know exactly which expenses it handles after a crash. UM/UIM policies cover bodily injury costs first and foremost, stepping in when the at-fault driver can’t pay. In California, you can also add uninsured motorist property damage (UMPD) coverage to protect your vehicle.

Medical costs and lost income

Your UM coverage pays for medical treatment resulting from the accident, including emergency care, surgeries, prescription medications, and rehabilitation. It also covers wages you lose while recovering from injuries that prevent you from working. Pain and suffering damages fall under UM coverage as well, compensating you for physical discomfort and emotional distress caused by the collision.

UM benefits extend to passengers in your vehicle who suffer injuries when an uninsured driver causes the crash.

Vehicle damage and other expenses

UMPD coverage handles repair or replacement costs for your vehicle when an uninsured driver damages it. California caps UMPD at $3,500 per accident, and you’ll pay a deductible before coverage kicks in. If you carry collision coverage on your auto policy, you might skip UMPD since collision provides broader protection for vehicle damage regardless of who caused the accident.

What California law requires and offers

California law mandates that insurers offer UM/UIM coverage to every driver who purchases auto insurance, but you’re not legally required to accept it. When you buy a policy, your insurer must present uninsured and underinsured motorist coverage in writing, and you can only decline it by signing a rejection form. Understanding what is uninsured motorist coverage helps you make this decision wisely.

The automatic offer requirement

Your insurance company must offer you UM/UIM limits that match your liability coverage limits, up to the policy maximum. If you carry $100,000 in liability coverage per person, your insurer offers the same amount in UM/UIM protection. You can choose lower limits or reject coverage entirely, but declining this protection leaves you vulnerable when uninsured drivers cause accidents.

California requires insurers to renew your UM/UIM coverage automatically each policy period unless you sign a new rejection form. This legal safeguard prevents coverage from lapsing without your explicit consent.

Most California drivers accept UM/UIM coverage because the premium increase is minimal compared to the financial protection it provides.

Optional property damage coverage

You decide whether to add uninsured motorist property damage protection separately from bodily injury coverage. UMPD carries a $3,500 cap and requires a deductible, making collision coverage a better choice for comprehensive vehicle protection.

How UM and UIM claims work after a crash

Filing a UM or UIM claim differs from standard liability claims because you’re seeking compensation from your own insurance company, not from the at-fault driver’s insurer. After a crash with an uninsured or underinsured motorist, you need to notify your carrier promptly and provide evidence that the other driver caused your injuries. Understanding what is uninsured motorist coverage includes knowing how these claims unfold in practice.

The notification and investigation process

Contact your insurance company within the timeframe specified in your policy, typically within 24 to 72 hours after the accident. Your insurer investigates whether the at-fault driver was truly uninsured or carried insufficient coverage. You’ll need to provide a police report, medical records, and proof of the other driver’s insurance status (or lack thereof). California law requires insurers to acknowledge your claim within 15 days and accept or deny it within 40 days after receiving all documentation.

Your own insurance company may investigate your claim as thoroughly as they would defend against a third-party claim.

Settlement negotiations with your own insurer

Your insurer evaluates your medical expenses, lost wages, and pain and suffering to determine a settlement offer. If you disagree with their valuation, you can negotiate or pursue binding arbitration as outlined in your policy. Unlike liability claims, UM/UIM disputes typically resolve through arbitration rather than litigation.

How much UM and UIM coverage to buy in CA

Deciding how much uninsured motorist coverage to carry requires balancing premium costs against your financial vulnerability after a crash. Most insurance agents recommend purchasing UM/UIM limits that match your liability coverage amounts, creating symmetrical protection. When you understand what is uninsured motorist coverage protects, you can make informed choices about how much you need.

Match your liability coverage at minimum

Your UM/UIM coverage should equal your bodily injury liability limits as a baseline. If you carry $100,000 per person and $300,000 per accident in liability coverage, purchase the same amounts in uninsured motorist protection. This matching approach ensures you receive the same level of protection whether an insured or uninsured driver injures you.

California insurers must offer UM/UIM coverage equal to your liability limits, making this symmetrical protection easy to obtain.

Account for your assets and medical risks

Consider purchasing higher UM/UIM limits if you own significant assets like a home or rental properties. Medical costs for serious injuries frequently exceed $100,000, and you want coverage that protects both your immediate medical needs and your long-term financial security. Drivers who commute long distances or frequently travel on congested highways face elevated exposure to uninsured motorists and should weigh increased coverage limits accordingly.

Next steps if you were hit by an uninsured driver

Getting hit by an uninsured driver creates immediate financial pressure, but you can take specific steps to protect yourself. File a police report within 24 hours and document everything: photos of vehicle damage, witness contact information, and your injuries. Contact your insurance company immediately to report the accident and determine whether you carry UM/UIM coverage.

Your next priority involves securing medical attention even if you don’t feel injured right away. Soft tissue damage and internal injuries often manifest hours or days after impact. Gather all medical records and repair estimates to support your claim.

If you’re struggling with what is uninsured motorist coverage claims or the at-fault driver’s insurer denies responsibility, legal representation becomes critical. Steven M. Sweat, Personal Injury Lawyers, APC has recovered hundreds of millions for California accident victims over 25 years. Contact our Los Angeles team for a free consultation about your UM/UIM claim.