- Free Consultation: 866-966-5240 Tap Here To Call Us

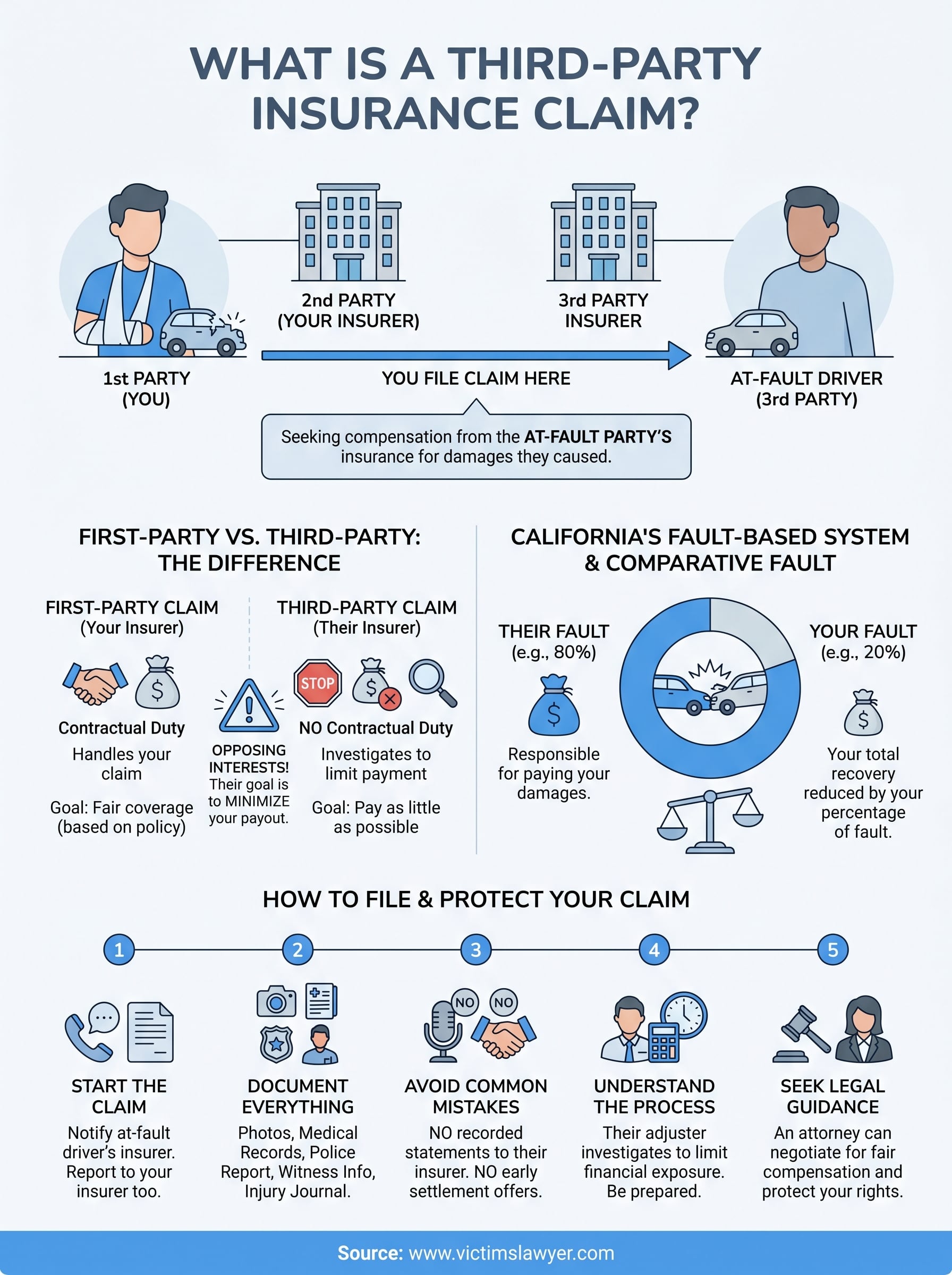

What Is a Third Party Insurance Claim? After an Accident

Quick Answer: A third-party insurance claim is a claim you file against the at-fault party’s insurer — not your own insurer, which would be a first-party claim. After a California car accident, this is how you recover for vehicle damage, medical bills, and pain and suffering from the driver who caused the crash. Because the at-fault insurer is not on your side, initial offers are often low.

Article Summary: A third-party insurance claim occurs when an individual seeks compensation from the insurance provider of another party who caused their accident or injury. In California’s fault-based system, this process is fundamentally different from first-party claims because the opposing insurer has no contractual obligation to look out for the victim’s best interests. Instead, adjusters often prioritize minimizing payouts through lowball settlement offers and aggressive negotiation tactics. To protect their rights, claimants must understand the state’s pure comparative negligence rules, which allow for recovery even if they share partial blame for the incident. Success depends on gathering comprehensive evidence, such as medical records, police reports, and accident scene documentation, while avoiding recorded statements that could be used to devalue the claim. Because accepting a settlement release permanently waives the right to future compensation, it is vital to wait until the full extent of injuries is known. Navigating these complexities within California’s two-year statute of limitations typically requires professional legal guidance to ensure victims recover sufficient funds for medical bills, lost wages, and long-term rehabilitation.

If someone else caused your accident, you probably aren’t supposed to file a claim with your own insurance company, you’re supposed to file one with theirs. That’s the core of what is a third party insurance claim, and understanding how it works can make a real difference in how much compensation you actually recover. It’s also one of the most common points of confusion for people dealing with injuries after a crash or incident in California.

A third-party claim is fundamentally different from a first-party claim, both in who you’re dealing with and in how the process plays out. The other driver’s insurance company has no obligation to look out for your interests, their goal is to pay as little as possible. That’s exactly why our team at Steven M. Sweat, Personal Injury Lawyers, APC has spent over 25 years helping accident victims in Los Angeles and throughout California fight back against lowball offers and stall tactics from opposing insurers.

This article breaks down what a third-party insurance claim is, how it differs from a first-party claim, the steps involved in filing one, and what you should know to protect your right to fair compensation after an accident caused by someone else’s negligence.

What a third-party insurance claim means

When you ask what is a third party insurance claim, the answer starts with understanding how insurance labels the people involved. In any insurance arrangement, “first party” refers to you as the policyholder, and “second party” is the insurance company you have a contract with. The “third party” is anyone outside that two-party agreement, most often the person who caused your accident and the insurer that covers them. Filing a third-party claim means you are seeking payment from someone else’s policy because their insured caused you harm.

First-party vs. third-party: the key difference

A first-party claim means you file directly with your own insurance company after a covered loss, regardless of who was at fault. A third-party claim means you file with someone else’s insurance company because their policyholder caused your injury or property damage. The distinction matters in a practical way: your insurer has a contractual duty to handle your claim fairly, while the at-fault party’s insurer has no such obligation to you. Their adjusters are trained to limit payouts, not to make sure you walk away with what you actually need.

The at-fault driver’s insurance company is not on your side. Its job is to protect its client’s policy, not to make sure you’re fairly compensated.

Who counts as a “third party”

The third party in a claim is most commonly the at-fault driver in a car accident, but the category is broader than that. In California, any person or entity whose negligent or reckless conduct leads to your injury can be the subject of a third-party claim. Common examples include:

- A negligent driver who ran a red light

- A property owner who failed to fix a hazardous condition

- A business whose employee caused harm while working

- A contractor whose work created a dangerous situation

You file against their liability coverage, and any compensation you receive comes from their policy limits rather than your own.

Why third-party claims matter after an accident

Understanding what is a third party insurance claim goes beyond a definition. It directly affects how much money you recover and whether your medical bills, lost wages, and pain and suffering get covered after an accident someone else caused. When you know how third-party claims work, you are in a stronger position to protect your rights from day one.

The financial stakes are real

After an accident, your costs can pile up fast. Medical treatment, rehabilitation, and lost income can far exceed what you initially expect. A third-party claim against the at-fault party’s policy is often your only realistic path to recovering those expenses without going out of pocket.

If you settle your third-party claim too early, you may waive your right to future compensation even if your injuries turn out to be more serious than initially diagnosed.

Why the other insurer’s interests conflict with yours

The at-fault driver’s insurance company has one primary goal: pay out as little as possible. Their adjusters are trained negotiators who know how to minimize settlements, not maximize your recovery.

Accepting an early offer without knowing the full extent of your injuries is one of the most costly mistakes you can make. Your damages often include future medical costs and lost earning capacity that are not visible in the first days after an accident.

How a third-party claim works in California

California follows a fault-based system, which means the person responsible for causing your accident is also responsible for paying your damages. When you understand what is a third party insurance claim in this context, you realize that your first step after an accident is establishing who was at fault, because fault determines which insurer you pursue and how much you can recover.

California’s comparative fault rule

California uses pure comparative negligence, meaning you can still recover compensation even if you were partly at fault. However, your total recovery is reduced by your percentage of fault. For example, if you were 20 percent at fault, you can only recover 80 percent of your total damages. This rule gives the opposing insurer a strong incentive to argue that you share blame, which is one more reason to document everything carefully from the start.

The less fault the opposing insurer can assign to you, the more your claim is worth, so never admit fault at the scene or in early conversations with adjusters.

What the insurer does after you file

Once you file, the at-fault driver’s insurer assigns an adjuster to investigate your claim. That adjuster will review the police report, gather statements, and assess your damages, all with the goal of limiting their financial exposure, not protecting your interests.

How to file and document a third-party claim

Filing a third-party claim starts the moment you decide to seek compensation from the at-fault party’s insurer. How you handle the first 24 to 72 hours after an accident directly shapes the strength of your claim, so acting quickly and methodically gives you a clear advantage.

Steps to start your claim

You begin by notifying the at-fault driver’s insurance company that you are filing a claim against their policyholder’s liability coverage. Gather the other driver’s insurance information at the scene if you can. Then report the accident to your own insurer as well, since many policies require it.

Do not give a recorded statement to the at-fault driver’s insurer without first speaking to an attorney, because those statements are used to limit your payout.

What documentation you need

Understanding what is a third party insurance claim also means knowing what evidence supports it. Strong documentation is the backbone of any successful claim. You should collect and preserve the following:

- Photos and videos of the accident scene, vehicle damage, and your visible injuries

- The official police report and incident number

- All medical records and bills tied to the accident

- Witness contact information and written statements where possible

- A personal injury journal tracking your symptoms and recovery day by day

Common issues and how to protect your claim

Once you understand what is a third party insurance claim, you quickly realize that filing one puts you up against a company whose interests are directly opposed to yours. Insurance adjusters use specific strategies to reduce or deny your payout, and knowing those strategies in advance gives you a real advantage.

Common tactics insurers use against you

The opposing insurer may contact you quickly after the accident with a settlement offer before you know the full scope of your injuries. They may also dispute liability, argue that your injuries were pre-existing, or use your own recorded statements against you. Accepting any offer before your treatment is complete almost always leaves money on the table.

Once you sign a settlement release, you cannot reopen your claim, even if your condition worsens later.

Steps to protect your claim

Avoid speaking directly with the at-fault driver’s adjuster without legal guidance first. Keep every receipt, medical record, and piece of communication tied to the accident organized in one place. If the insurer denies your claim or offers far less than your actual damages, an experienced personal injury attorney can negotiate on your behalf or take the case to litigation if necessary. Acting early puts you in the strongest possible position to recover what you are owed.

Next steps

Now that you understand what is a third party insurance claim, you have the foundation to make smarter decisions after an accident caused by someone else. The opposing insurer will move fast to protect its client’s money, and your response in the early days shapes how much you ultimately recover. Document everything, avoid giving recorded statements, and do not accept any settlement before your treatment is complete and your total losses are clear.

Personal injury claims in California involve real legal deadlines, and missing them means losing your right to compensation entirely. The statute of limitations for most personal injury cases in California is two years, but certain circumstances can shorten that window significantly. Getting a legal opinion early costs you nothing and puts you in the strongest position possible. If you were injured because of someone else’s negligence, speak with our team today to get a free consultation and understand your full legal options.