- Free Consultation: 866-966-5240 Tap Here To Call Us

What Does Uninsured Motorist Insurance Cover In California?

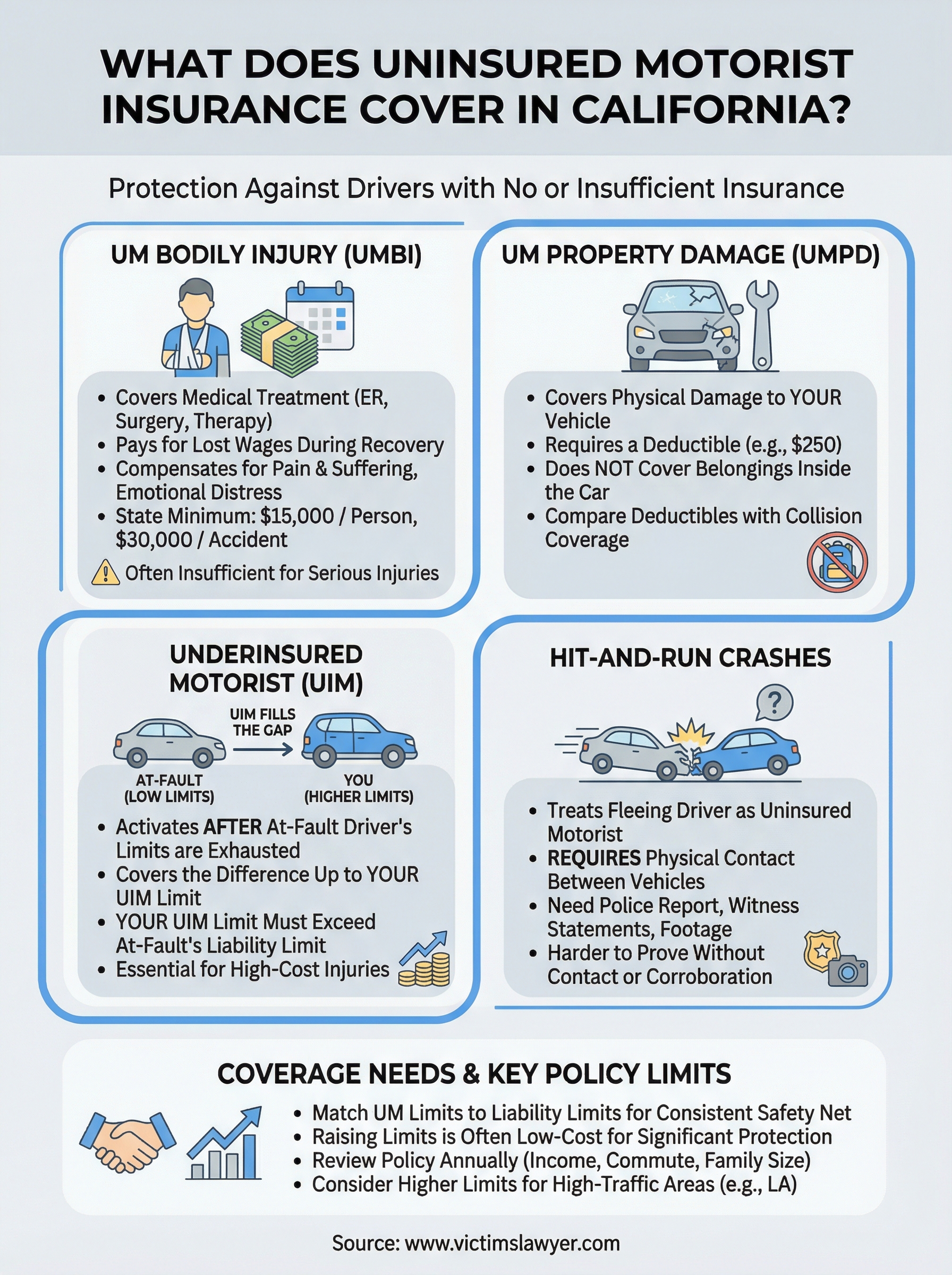

Article Summary: With roughly one in seven California drivers operating without insurance, uninsured motorist (UM) coverage serves as a vital financial safeguard for responsible motorists. This protection consists of two primary components: bodily injury (UMBI) and property damage (UMPD). UMBI addresses medical expenses, lost wages, and non-economic harms such as pain and suffering, while UMPD handles vehicle repairs, typically subject to a $250 deductible. Additionally, underinsured motorist (UIM) coverage bridges the gap when an at-fault driver’s policy limits are too low to cover total damages. In hit-and-run scenarios, UM coverage generally requires proof of physical contact and a formal police report to apply. However, UM insurance does not cover property besides the vehicle or liability for injuries caused to others. Because California’s minimum limits of $30,000 per person and $60,000 per accident are often insufficient for serious collisions, experts recommend matching UM limits to personal liability thresholds. Navigating these claims remains complex, as insurers frequently attempt to minimize payouts, making professional legal guidance from firms like Steven M. Sweat, Personal Injury Lawyers, APC essential for ensuring victims receive the full compensation they are legally owed following a crash.

About one in seven drivers on California roads has no auto insurance at all. If one of them hits you, your own policy may be the only thing standing between you and tens of thousands of dollars in out-of-pocket costs. That raises a critical question: what does uninsured motorist insurance cover, and is your current policy enough to protect you? Understanding the answer could be the difference between financial recovery and financial ruin after a serious collision.

At Steven M. Sweat, Personal Injury Lawyers, APC, we’ve spent over 25 years representing injured Californians, many of whom didn’t realize until after a crash that the at-fault driver carried zero coverage. We’ve seen firsthand how uninsured motorist (UM) claims interact with personal injury cases, and how the right coverage can keep victims from absorbing costs that should never be theirs. Our Los Angeles-based team handles these disputes daily, fighting insurers who try to minimize or deny legitimate UM claims.

This article breaks down exactly what UM insurance pays for in California, how it differs from underinsured motorist (UIM) coverage, and whether adding or increasing this protection makes sense for your situation.

What uninsured motorist coverage pays for in California

Uninsured motorist coverage steps in when a driver who caused your accident carries no liability insurance at all. Understanding what does uninsured motorist insurance cover clarifies why this protection matters: in California, it comes in two distinct forms: UM bodily injury (UMBI) and UM property damage (UMPD). Both protect you from absorbing costs that should legally belong to the at-fault driver, and both are offered by insurers as a package you can accept or waive in writing.

Medical expenses and lost income

UMBI pays for the medical treatment you need as a direct result of the crash. That includes emergency room visits, surgeries, physical therapy, prescription medications, and follow-up specialist care. If your injuries force you to miss work, UMBI also covers lost wages during your recovery period. California requires insurers to offer UM coverage at minimum limits of $15,000 per person and $30,000 per accident, though those amounts rarely cover serious injuries in full.

If your combined medical bills and lost income exceed your UM policy limit, you absorb the remaining balance out of pocket, which is exactly why carrying only the state minimum carries real financial risk.

Pain, suffering, and property damage

Beyond the financial losses you can tally on a spreadsheet, UMBI compensates you for non-economic harms that are harder to quantify. Common examples of what your policy covers in this category include:

- Pain and suffering from the injury itself

- Emotional distress and anxiety following the crash

- Loss of enjoyment of daily activities

- Permanent disfigurement or long-term disability

UMPD covers physical damage to your vehicle when an uninsured driver hits it, though California law requires a $250 deductible on every UMPD claim. If you already carry collision coverage, compare the deductibles on both before deciding which to use, because the better financial choice depends on your specific policy terms.

Underinsured motorist coverage and how it differs

Underinsured motorist (UIM) coverage addresses a different gap than UM coverage does. Here, the at-fault driver carries insurance, but their policy limits fall short of covering your actual damages. California law requires insurers to offer UIM coverage alongside UM coverage, and understanding both answers a significant part of what does uninsured motorist insurance cover in practical terms.

How UIM kicks in after a crash

Your UIM coverage activates after the at-fault driver’s liability insurer pays out their full policy limit. If that driver carries only $30,000 in bodily injury coverage but your medical bills total $80,000, your UIM policy covers the remaining gap up to your own UIM limit.

Your UIM limit must exceed the at-fault driver’s liability limit for your coverage to pay anything at all under California law.

Why carrying higher UIM limits matters

California allows insurers to sell UIM coverage in amounts that match your UM limits, and many drivers leave both at the state minimum. Raising both limits together increases your protection without dramatically increasing your premium, and it ensures you have a meaningful safety net when a minimally insured driver causes serious, high-cost injuries that a bare-minimum policy simply cannot absorb.

When UM coverage applies in hit-and-run crashes

Hit-and-run crashes are one of the most frustrating scenarios an accident victim faces. The driver who caused your injuries disappears, leaving you with no liable party to pursue and no insurance policy to file against. This is where UM coverage fills a critical role, treating the unknown hit-and-run driver as an uninsured motorist under California law.

The physical contact requirement

California insurers generally require actual physical contact between the hit-and-run vehicle and your car before your UM policy will pay out. If a driver cuts you off and forces you to swerve into a barrier without ever touching your vehicle, proving your claim becomes significantly harder without corroborating witness testimony.

Document the scene thoroughly, report the crash to police immediately, and gather any witness contact information, because these steps directly affect whether your UM claim succeeds.

Reporting and proof standards

Your insurer will ask for a police report filed promptly after the incident, along with any available surveillance footage or witness statements. Meeting these documentation requirements strengthens your claim and prevents the insurer from using gaps in your evidence as grounds to deny or reduce what does uninsured motorist insurance cover under your specific policy terms.

What UM coverage does not pay for

Understanding what does uninsured motorist insurance cover requires equal clarity about what falls outside its scope. UM coverage is not a catch-all policy, and knowing its specific exclusions prevents costly surprises when you file a claim after a crash.

Property damage gaps

UMPD does not cover your vehicle if you are fully or partially at fault for the collision. California law also excludes UMPD from covering damage to property other than your car, such as personal belongings inside the vehicle at the time of the crash. If the at-fault driver is uninsured but you share a portion of the blame, your UMPD payout may be reduced proportionally under California’s comparative fault rules.

UMPD will also pay nothing if you waived that specific coverage in writing when you purchased your policy, a step many drivers take without fully weighing the financial risk.

Medical and liability exclusions

UMBI does not cover injuries you cause to other people, regardless of whether the other driver carried insurance. Your UM policy covers only you and your passengers when an uninsured driver is responsible. Additionally, your UM policy does not replace a workers’ compensation claim if the crash happened while you were performing job-related duties, because workers’ comp typically takes priority and governs those injuries under a separate legal framework.

How much UM coverage you need and key policy limits

California sets the minimum UM coverage at $30,000 per person and $60,000 per accident, but those limits rarely cover serious injuries in full. Understanding what does uninsured motorist insurance cover at minimum versus higher thresholds helps you choose a policy that actually protects your financial recovery.

Matching your UM limits to your liability limits

Your insurer cannot sell UM coverage that exceeds your liability limit, but matching the two figures gives you a consistent safety net on both sides of any crash. Most drivers find that raising both limits together adds relatively little to their annual premium while dramatically increasing the protection available when they need it most.

Raising your per-person UM limit from $15,000 to $100,000 typically costs far less per year than most drivers expect.

Evaluating your personal risk exposure

Consider your income, medical history, and household size when setting your UM limits. Drivers who commute regularly through high-traffic Los Angeles areas face greater statistical exposure to uninsured motorists, which makes higher limits a practical choice rather than an unnecessary expense.

Reviewing your policy annually ensures your UM and UIM coverage keeps pace with changes in your income or family situation. A limit that felt sufficient two years ago may leave real gaps today if your financial circumstances have shifted.

What to do next

Now that you understand what does uninsured motorist insurance cover in California, the most important step is reviewing your current policy before another driver makes that coverage necessary. Pull your declarations page and confirm your UM and UIM limits, your deductible on UMPD, and whether you signed a waiver on any portion of this coverage without fully understanding what you gave up.

If an uninsured or underinsured driver has already hit you, do not navigate that claim alone. Insurers routinely offer less than your policy entitles you to, especially when you are unrepresented and unfamiliar with how California’s UM laws apply to your specific losses. The attorneys at Steven M. Sweat, Personal Injury Lawyers, APC have handled hundreds of UM disputes and know exactly where insurers cut corners. Your consultation is free and carries no obligation, so reach out today and let us review your claim: contact our Los Angeles personal injury team.